It's been a little while since I've written a proper Captain's Log, and this one came out of a situation that hit a nerve. Not a big, life-altering event, just one of those small things that makes you stop and say, "Wait a minute... that's not right." And sometimes those little moments are the best ones to talk about, because they happen to all of us more often than we'd like to admit.

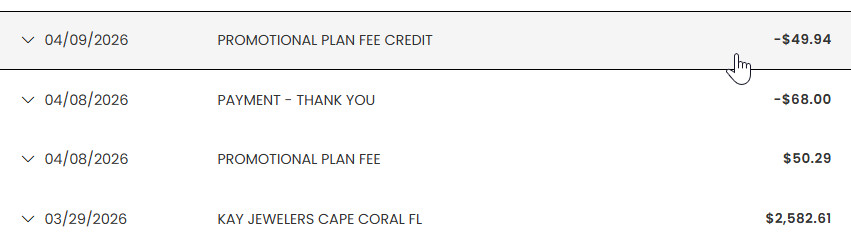

So here's what happened. I recently bought something nice for my wife from Kay Jewelers. Nothing unusual there. I've shopped with them before, used their store card, taken advantage of their promotional financing, and always paid everything on time. No issues. No surprises. I like promotional financing because some stores will give you a discount if you use their card at their store. Walmart, for example, does this. My Kay's card gave me 6-12 months interest-free, which was great. I could buy something cute for the wife, and then I've got 6 months to pay it off. So I bought her something cute. Then I get my statement and see a $50 charge labeled "Promotional Plan Fee." That immediately triggered my internal red alert (1). My first thought was simple: what fee?

I reached out to them through their messaging system, and at first I got the usual "please call us" response. Not happening. If you've followed me for any amount of time, you know I don't do phone calls unless someone is offering me a starship and a warp drive. So I pushed back and kept everything in writing, which is what I prefer to do, especially for things like this where I want everything documented in writing. Eventually, they explained that this was a new 2% fee tied to promotional financing, something they said was disclosed in a prior statement under a "Change in Terms" notice. And there it is. The classic fine print defense, buried where almost nobody sees it.

Now, let's be honest. Who actually reads every line of every statement that comes in, especially when there's no balance or activity? That's not how normal humans operate. If you're introducing a new fee that directly affects a purchase decision, that needs to be disclosed clearly at the time of sale. Not tucked away in a document that most people skim at best. That's not transparency. That's hoping nobody notices. And that's where I draw the line on ethics. That's kind of like software terms of service, right? No one ever reads it - they just scroll to the bottom and click accept. This is a situation where software you've used for years suddenly sneaks in a change and makes you click Accept again without telling you what that change is specifically.

To their credit, after a bit of back and forth, they did reverse the charge. So this isn't a horror story about a company refusing to fix a mistake. It's more about the principle behind it. Because even though they made it right for me, the system itself is still in place. That fee is still there, waiting for the next person who doesn't catch it or doesn't feel like pushing back. And that's where this turns into a broader conversation about awareness.

One of my core rules when it comes to money is simple. I use credit, but I use it smartly. I don't buy things I can't afford. If I can't pay it off before interest kicks in, I don't buy it. Period. Credit cards are tools, not lifelines. Used correctly, they're incredibly powerful. Used incorrectly, they'll dig a hole faster than a Ferengi with a shovel searching for buried gold. I'll take 3% cash back, but I won't pay 29% interest on a purchase for something that I don't really need.

Here's the part that really made me shake my head. If a promotional plan now comes with a 2% fee, why would I use it? I've got other cards that give me 3% or 4% cash back on purchases. I can put the same purchase on something like my American Express Platinum Card, pay it off quickly like I always do, and actually come out ahead instead of paying for the privilege. At that point, the "promotion" isn't a benefit. It's a cost.

At the end of the day, this didn't cost me anything. I got the fee reversed, lesson learned, moving on. But it did reinforce something I already believe strongly. You have to stay aware. You have to question things that don't look right. And you have to be willing to push back when something feels off, even if it's "just fifty bucks." Because those little things add up, and more importantly, they set the tone for how companies treat their customers. I try to take care of all my customers as best I can. If you ever notice anything out of whack with my billing, then you let me know and I'll make it right.

So now I'm curious. Have you ever caught a fee like this on a statement that made you stop and go, "Wait... what is that?" And did you let it go, or did you fight it?

Here's the email chain, for those of you who care:

Details--- BEGIN EMAIL CHAIN ---

From: You

Sent: Thursday, April 9, 2026, 4:33 PM (ET)

To: Comenity Bank

Subject: Late Fees or Finance Charges

Message ID: 248334213

I was charged a $50.29 "Promotional Plan Fee" and need to know what this is. I've always paid my promo balances on time and was not told of any fees when selecting the deferred plan. If this fee is tied to that plan, remove me from it. I'll pay the balance in full next cycle. Please review and reverse this charge or explain it. You guys have never charged me a promotional fee in the past, and I have always paid my balances by the date due.

From: Comenity Bank

Sent: Sunday, April 12, 2026, 5:18 AM (ET)

To: You

Subject: Re: Late Fees or Finance Charges

Message ID: 248448889

I am with Comenity Bank, which handles your credit card account. I'm here to help with your account needs.

Thank you for contacting us.

We're implementing this promotional plan transaction fee to continue to offer special credit financing that provides a broad base of customers with more flexibility when paying back their loans.

I see the account was charged a promotional plan transaction fee for a purchase put on a promotional plan, and I am happy to explain. The fee of $50.29 is for the purchase made on 03/29/2026. The fee is 2% of the purchase that was placed on the promotional plan, sometimes also referred to as special financing.

Thank you for taking the time to reach out, and have a great day.

Sincerely,

N. Sultana

Internet Customer Care Team

From: You

Sent: Tuesday, April 14, 2026, 6:51 PM (ET)

To: Comenity Bank

Subject: Re: Late Fees or Finance Charges

Message ID: 248510786

Thank you for the explanation, but this does not resolve the issue. I was never informed at the time of purchase that selecting the promotional financing would include a 2% fee, and I would have declined it if I had been. This was not disclosed by the sales associate, and burying it in fine print is not adequate. I have used promotional financing before and have never been charged a fee, and I have always paid on time and in full. I am requesting that the $50.29 fee be removed. If it is not, I will close this account and no longer use this card or make purchases through Kay Jewelers.

From: You

Sent: Thursday, April 16, 2026, 5:44 PM (ET)

To: Comenity Bank

Subject: Re: Late Fees or Finance Charges

Message ID: 248564335

Still waiting for a reply to my inquiry.

From: Comenity Bank

Sent: Friday, April 17, 2026, 6:44 PM (ET)

To: You

Subject: Re: Late Fees or Finance Charges

Message ID: 248587090

I am with Comenity Bank, which handles your credit card account. I'm here to help with your account needs.

We apologize for any inconvenience you may have experienced.

Please give us a call.

For us to best assist you with this concern, we ask that you speak with a live representative. Please call our Customer Care team at 1-855-506-2499 at your earliest convenience.

Thank you for being attentive to your account and taking the time to reach out. Have a great day.

Sincerely,

R. C.

Internet Customer Care Team

From: You

Sent: Sunday, April 19, 2026, 1:49 AM (ET)

To: Comenity Bank

Subject: Re: Late Fees or Finance Charges

Message ID: 248624681

I appreciate you getting back to me, but I absolutely hate making phone calls and I do not wish to contact your customer care team.

My issue is very simple and can be handled here in your secure messaging center. I recently made a purchase and was not informed in the store that there would be a 2% promotional charge. I've made many purchases from Kay in the past and have NEVER been charged a fee. If that information was buried in fine print, that is not ethical and likely not legal. I would not have agreed to any promotional charge and would have used a different credit card.

My position is straightforward: remove the promotional charge from my account, or I will pay the balance in full and consider this account closed. I am not going to spend time calling an 800 number to resolve something that can be handled right here.

If you choose to honor my request, great. If not, please consider this the end of my relationship with your company, and with Kay.

From: Comenity Bank

Sent: Tuesday, April 21, 2026, 3:28 PM (ET)

To: You

Subject: Re: Late Fees or Finance Charges

Message ID: 248691248

I am with Comenity Bank, which handles your credit card account. Your inquiry has been escalated to me for further review.

I'm sorry to upset you - we don't take your feedback lightly.

Knowing what matters to you is how we can improve, so I'll be sure to pass along your concerns.

You may remember we sent you a Change-in-Terms notice in a previous statement.

That document explained promotional plan transaction fees, which are a common practice with credit cards. It also mentioned the 2% fee we recently introduced on promotional plan purchases.

This fee allows us to continue to offer special credit financing that provides a broad base of customers with more flexibility when paying back their loans.

We charge the fee at the start of the plan. If you return part of a promotional plan purchase, the fee may be adjusted. If you return the entire purchase, we will credit the entire fee to your account.

We value your business and do not wish to lose you as our valued customer.

Please be assured that the promotional plan fee for $50.29 has been credited to your account. You can expect to see the credit applied to your account in 2-3 business days.

If you have any questions, please click the reply button.

Sincerely,

Y. Pandey

Internet Customer Care Team

From: You

Sent: Tuesday, April 21, 2026, 5:57 PM (ET)

To: Comenity Bank

Subject: Re: Late Fees or Finance Charges

Message ID: 248692676

Thank you for taking care of this and issuing a credit. I appreciate the resolution. I understand a Change-in-Terms may have been in a prior statement, but those are easy to miss. Had I known about the 2% promotional fee at purchase, I would not have accepted the financing. I have used this card for years and have never seen a fee like this. This type of charge should be clearly disclosed by the sales associate AT THE TIME OF SALE, not buried in fine print. Without upfront disclosure, it can easily catch customers off guard, which I do not think is appropriate or ethical. Thank you for clarifying how this works going forward.

However, if promotional financing now includes a fee, it reduces the value of using this card. I can get 4% cash back with other cards, such as my Amex Platinum, and I typically pay balances quickly anyway. I will continue shopping with Kay Jewelers, but will likely not use this card going forward. Thank you again.

--- END EMAIL CHAIN ---

Matt Hall

@Reply 2 months ago

Doesn't that render their card useless for saving money if using it someone is going to pay either interest...or a promotional fee? Either way, they forfeit the cash back they could get with the other cards. I mean, with 2% for 6 months same-as cash, they are essentially paying 4% APR instead plus the 4% they could have gotten back with the other card.

Matt exactly. That's what I said to them: why should I bother using your card and pay 2% when I can use another card and get 3% cash back? It doesn't make sense. They're going after people with low or no credit who are like, "Oh, wow, great, I can get this credit card and have 12 months to pay off this gift for Mom or whatever." If you've got decent credit, it's a complete waste.

Thomas Gonder

@Reply 2 months ago

Subscription charges from platforms like Google and others have become frustratingly difficult to manage. Recently, I was charged by an old program I no longer use, and there was no clear or accessible way to cancel the subscription.

There should be a law requiring companies to send a notification email at least 10 days before a subscription renews. That email should clearly state the upcoming charge and provide straightforward instructions or a direct link for canceling the subscription. This would give users a fair opportunity to review and stop charges they no longer want.

Lisa Snider

@Reply 2 months ago

Well, that's not likely to happen with this administration. They've gutted the CPB after all.

Ahh...the promo-credit promo fee. It's probably in the fine-fine print.

Michael Olgren

@Reply 2 months ago

I'm afraid I'm a little more cynical here... The billionaires and corporate American have won. The little guy can only beat them rarely and with Herculean effort. They put in "dark paths" like this to nickel and dime us because they know many of us will not notice or will not bother to fight it.

I value my time somewhere around $100 per hour. It takes about an hour to mow my lawn. If I could find someone to mow it for <$100, I'd hire them. I cannot, so I do it. When some company hits me with a bogus, unethical fee as you have described, it'll often take an hour on the phone, usually putting me in a bad mood and raising my blood pressure. Yes, I should fight it, but I'm afraid I usually don't. They've won. As the news recently pointed out, the top 1% own 50% of ALL the stock shares. It's like dealing with a contractor or medical office on Cape Cod. They're fine to lose your business because they already have more business than they can handle.

Sorry to be a downer but resigning myself to it saves me all kinds of cardiac arterial inflammation.

You can't find someone to mow your lawn for less than $100? I pay $140 / month for a company to mow my lawn. And that's weekly during the summer rainy months and biweekly in the dry season. Takes them like 20 minutes, and that includes edging, weeding, trimming bushes, etc.

But I feel ya... sometimes the fight ain't worth it. I find, however, that the older I get, the more I want to win just for the sake of winning, and not letting those bastards get away with it. Is the $50 promo fee worth the hour or so I wasted emailing them back and forth? Probably not.

But it's the principle.

Michael Olgren

@Reply 2 months ago

Per Zillow, the *median* home price on Cape Cod is $750K. Hard for folks who earn a lawn-mowing wage to live there. It's just under an hour to go "off Cape." So yeah, landscaping crews earn $50/hr which gets transmitted to me as >$100 to mow my small lawn. It takes me about 20 minutes on the Cape. The hour I quoted is here in Michigan (just bought 2nd house to be near my aging parents who need help and support). And tbh, I could probably get the neighbor's 16-yr old to do it for $50. Maybe.

First world problems, I know...

Michael Olgren

@Reply 2 months ago

And to show you how cheap I am... It would cost about $3,000 to pay someone to spread mulch at my Cape home, so I'll probably fly home for a long weekend and spread the $600 (15 yards) of mulch myself (did it last year).

Michael Yeah, I see what you mean about Cape Cod. We're here in Cape Coral where the median's around 400K, so it's still pretty reasonable by comparison.

The wife and I have actually been kicking around the idea of moving a little further south to Naples since a lot of the restaurants and stuff we like are out that way. But yeah... now we're stepping into the same territory you're talking about. You start seeing numbers more like 700K to a million depending on the area, and suddenly it's like, okay, maybe not just yet.

Might need to sell a few more videos and memberships first.

I'm the same way you are with the time vs money thing. If it's something I enjoy, I'll do it. I actually used to enjoy mowing the lawn back when I lived up in Buffalo. Cooler weather, nice grass, you could walk barefoot without worrying about stepping on something that wants to kill you. Down here... yeah, not so much. I love being outside, I love the heat and the humidity, I love hanging out in the pool, but doing yard work when it's 98 degrees and 80 percent humidity? Hard pass. I don't care what that costs. I'm paying someone to do it.

If it's something I don't want to do, then I consider it work. And I'd much rather do the WORK that I want to do, which is making videos, doing things that actually bring in money. On the flip side though, the older I get, the more I do find myself enjoying little projects around the house, so I get exactly where you're coming from there too.

Michael Olgren

@Reply 2 months ago

Richard It's funny you mention little projects around the house. This new house was left with a lot of unfinished work and weird mistakes. For example, there's a Cat 6 cable that runs from the cable box in the basement to the TV location in the living room. However, the end of the cable by the cable box is just the wire-- no RJ45 connector! I don't have a crimper but will have to figure that out. And the kitchen faucet had the hot and cold reversed from the "standard" connection. The connecting hoses were even labeled! Fortunately, an easy fix. There were no towel rings or toilet paper holders-- bought a drill driver and put those in. Next up are drawer pulls and cabinet knobs...

Matt Hall

@Reply 2 months ago

Michael Depending on what you want to do, amazon has a large variety of networking tools that I have had good luck with. Anything Ideal or Klein is going to be high quality.

If you just want to put a clear male end on the cable, you will want a crimper. I have Klein, Ideal, and off brands and they all work well. If you are using non-pass through connectors, you may also want a pair of side cut pliers or scissors to even up the ends of the conductors before inserting them into the connector.

If you want to attach a female that installs into a wall plate or patch panel and use a patch cable from there to the device, they refer to those as a "tombstone". For that you will want a 110 punchdown tool (one conductor at a time) or a tombstone crimper (8 conductors in one shot). I have an Everest brand tombstone crimper and it works well. I also have Ideal and Klein punch down tools they work fine but I prefer the tombstone crimper.

Either way you might consider a network test tool. They will tell you if any of the conductors aren't connected or are connected but out of order. I have a Kolsol NF-8209 and it works well.

Most networking I have run across is T568B configuration. It is worth a quick lookup for wire order. It is a little tedious to get started doing this work but is pretty easy once you get the basics down.

If you are a Visitor, go ahead and post your reply as a

new comment, and we'll move it here for you

once it's approved. Be sure to use the same name and email address.

This thread is now CLOSED. If you wish to comment, start a NEW discussion in

Captain's Log.